#48 - Atlas Engineered Products Valuation

Last updated: Nov 1, 2022

Since I shared my thoughts about $AEP.V previously and they just released their 2021Q4 earnings, I decided to update my valuation of the business.

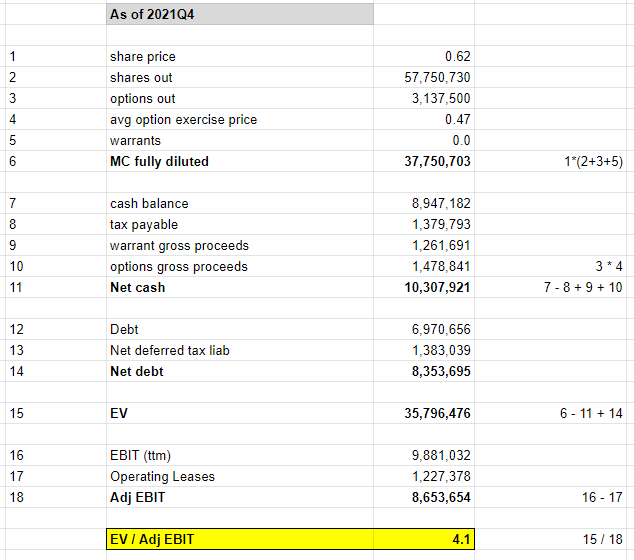

Here’s a screenshot below. The worksheet can be found here.

Note: I considered 100% of the deferred tax liability as debt (conservative assumption).

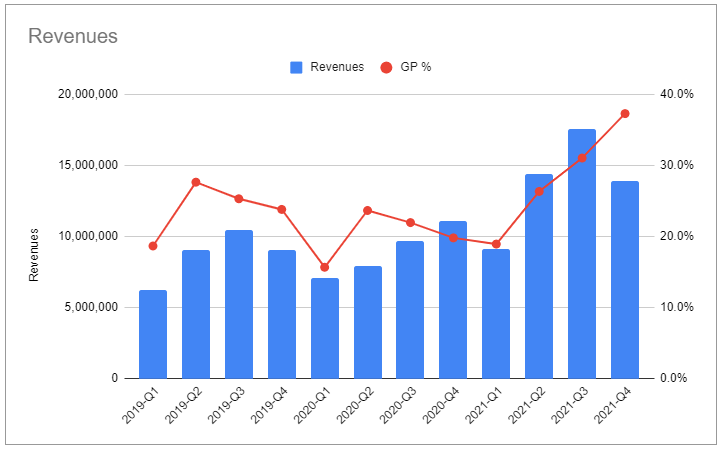

The business is probably not as undervalued as it seems here, given the concerns I shared before and more importantly, given how “particular” 2021 was.

The following chart shows this (pay attention to the gross profit margin):

I think AEP kind of stumbled upon these higher margins and they managed to keep them in 2021Q4. I doubt they’ll stay this high longer term.

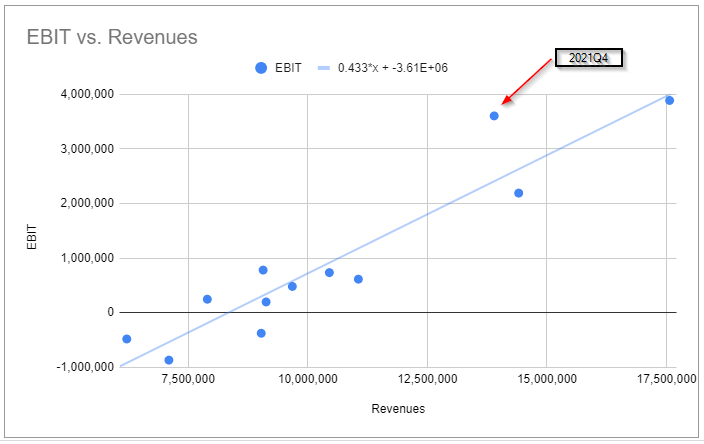

Finally, looking at a chart of EBIT vs Revenues for each quarter since 2019Q1, we see that the last quarter seems to be an outlier, and that the break-even is around $8.5M of quarterly revenue.

As I’ve said before, this is a significant position for me. I haven’t sold a share but I’m not expecting an amazing year for this business in 2022.

Disqus comments are disabled.